Your Guide to Managerial Accounting: Types, Careers, and More

These restrictions have a significant impact on both financial reporting and program management. Nonprofits must track restricted funds separately from unrestricted funds to maintain transparency and compliance. Additionally, understanding these distinctions aids in better planning and resource allocation, helping organizations align funding with program goals.

What replaced inflation as the top challenge for finance leaders

A copy of 11 Financial’s current written disclosure statement discussing 11 Financial’s business operations, services, and fees is available at the SEC’s investment adviser public information website – or from 11 Financial upon written request. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site.

Be the future of Accountancy and Tax

Economic exposure increases as foreign exchange volatility rises and decreases as volatility declines. It is usually created by macroeconomic conditions such as geopolitical instability and/or government regulations. Companies try to manage economic exposure to reduce the impact foreign currency volatility has on their cashflows. In this module, we introduce the role of costing systems, identify some example systems and settings in which they are most useful, and explore how accounting for overhead costs influences the value of cost information.

What are typical careers that use management accounting?

They’re critical executives and team members who are highly valued by the board and executive team. We collaborate with business-to-business vendors, connecting them with potential buyers. These financial relationships support our content but do not dictate our recommendations.

This means landing a managerial accounting position will give you an excellent opportunity to impress your team while building valuable skills and relationships. Busy professionals often choose self-paced programs that allow for part-time attendance; however, this typically lengthens completion time. This could include vacation placements, how sales commissions are reported in the income statement sandwich courses or part-time employment offering business experience. Relevant work experience may also count towards the three years of experience needed to begin the CIMA CGMA qualification route. The CIMA CGMA Professional Qualification consists of three levels, with each level made up of three exams and a case study test.

- Finance decision-makers in a quarterly survey say they have concerns on several fronts.

- Notably, strategic management accounting does not have a direct effect on organizational performance.

- Some of these universities also provide in-house training and examinations of the CMA program.

- Misunderstanding or mismanaging these distinctions can lead to compliance issues, strained donor relationships, and complications in financial reporting.

- Management accounting concentrations include additional courses in controllership, internal and operational auditing, accounting and reporting issues, and advanced management accounting.

Management makes decisions based on the data they have available, and these managerial accounting decisions give context to the data. A poorly structured selling and administrative expense budget can affect not just tactics but also strategy. Since managerial accounting is different than financial accounting, this goes beyond just revenues and expenses.

Transaction exposure typically arises from payments for imported goods and services or receipts of payments from foreign entities. Each institution determines the number of credits recognized by completing this content that may count towards degree requirements, considering any existing credits you may have. CPAs who want to drive greater profitability and growth must understand customer acquisition costs and customer lifetime value.

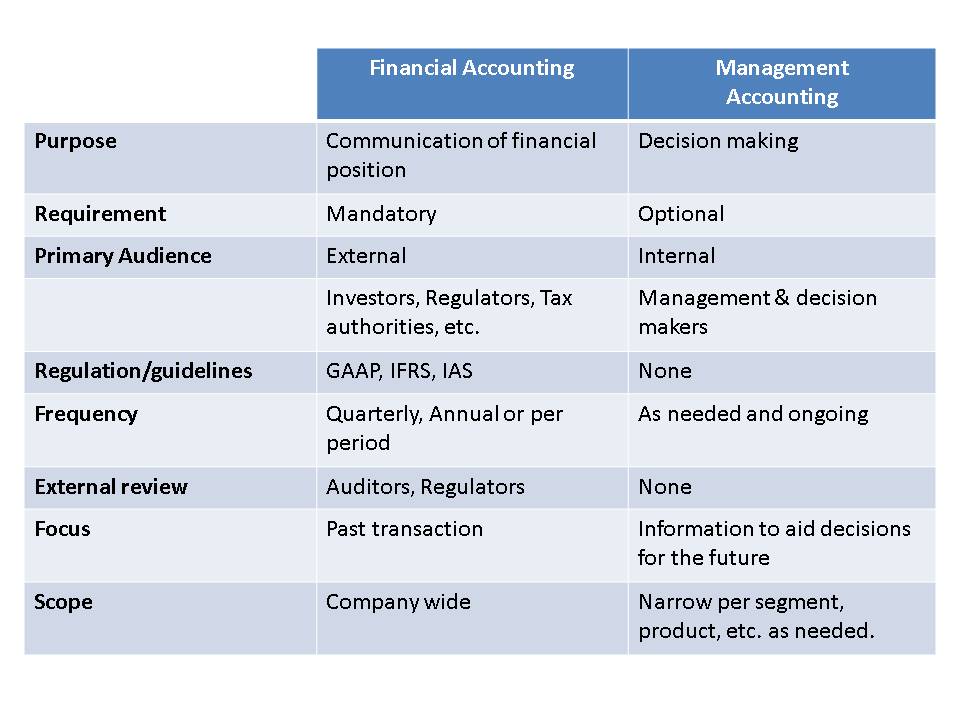

All publicly held companies are required to complete their financial statements in accordance with GAAP as a requisite for maintaining their publicly traded status. Most other companies in the U.S. conform to GAAP in order to meet debt covenants often required by financial institutions offering lines of credit. Activity-based costing also de-emphasizes direct labor as a cost driver and concentrates instead on activities that drive costs, as the provision of a service or the production of a product component. Variance analysis is a systematic approach to the comparison of the actual and budgeted costs of the raw materials and labour used during a production period. In management accounting or managerial accounting, managers use accounting information in decision-making and to assist in the management and performance of their control functions.

Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Management accountants produce dedicated reports to serve the needs of decision-makers.

Managerial accounting, in contrast, uses pro forma measures that describe and measure the financial information tracked internally by corporate managers. Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors. Managerial accounting is the practice of identifying, measuring, analyzing, interpreting, and communicating financial information to managers for the pursuit of an organization’s goals. The distinction between traditional and innovative accounting practices is illustrated with the visual timeline (see sidebar) of managerial costing approaches presented at the Institute of Management Accountants 2011 Annual Conference. To facilitate its educational objectives, the Institute has accredited a number of universities which have master’s degree subjects that are equivalent to the CMA program.